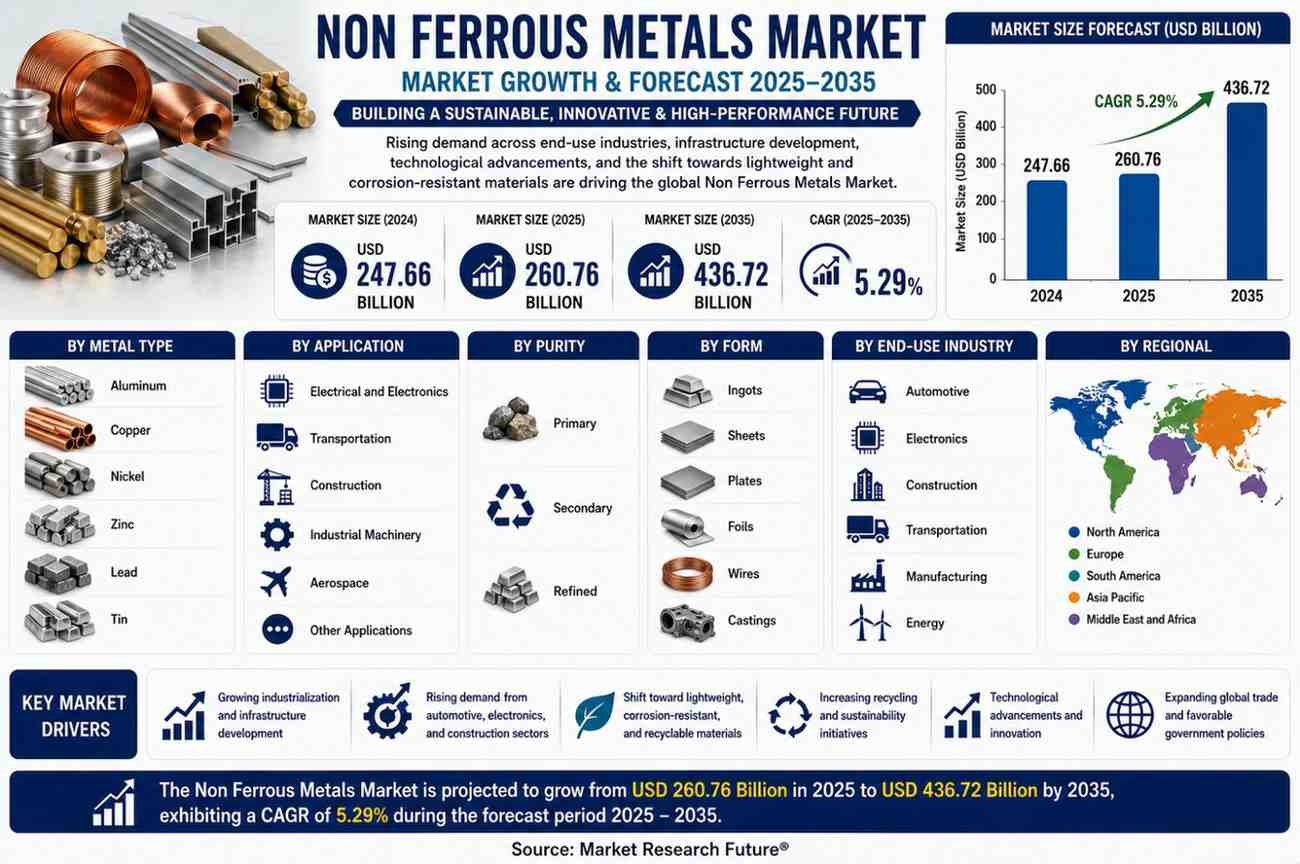

According to Market Research Future®, the Non Ferrous Metals Market was valued at USD 247.66 billion in 2024 and is projected to grow from USD 260.76 billion in 2025 to USD 436.72 billion by 2035, registering a compound annual growth rate (CAGR) of 5.29% during the forecast period (2025–2035). The market is entering a transformative decade driven by global electrification, accelerating renewable energy deployment, modernization of transportation infrastructure, and increasing adoption of lightweight engineering materials. As industries strive to improve energy efficiency while reducing carbon emissions, non-ferrous metals are becoming increasingly central to manufacturing, construction, automotive production, aerospace engineering, electronics, and clean energy technologies.

Market Overview

Non-ferrous metals form the backbone of numerous industrial ecosystems due to their exceptional combination of electrical conductivity, corrosion resistance, lightweight characteristics, thermal efficiency, ductility, and recyclability. Unlike ferrous metals, which primarily contain iron, non-ferrous metals such as aluminum, copper, nickel, zinc, lead, and tin deliver specialized performance characteristics required for advanced engineering applications.

These metals are indispensable across industries that demand high conductivity, reduced structural weight, long service life, and superior environmental resistance. From power transmission cables and semiconductor manufacturing to aircraft structures, electric vehicles, renewable energy installations, telecommunications equipment, and industrial machinery, non-ferrous metals enable technological advancement across virtually every modern economy.

The transition toward low-carbon infrastructure has further elevated the strategic importance of these materials. Governments worldwide continue investing heavily in renewable electricity generation, battery manufacturing, electric mobility, digital infrastructure, and industrial modernization. These investments are creating sustained demand for aluminum, copper, nickel, and other specialty metals while encouraging mining companies to expand production capacity and adopt environmentally responsible extraction technologies.

Market Size

The Non Ferrous Metals Market reached USD 247.66 billion in 2024 and is estimated to increase to USD 260.76 billion in 2025.

With a projected CAGR of 5.29% during the 2025–2035 forecast period, the market is expected to attain approximately USD 436.72 billion by 2035.

Steady industrial growth, expanding infrastructure investments, rising renewable energy deployment, and increasing adoption of electric mobility continue supporting this long-term growth trajectory.

2025 Market Analysis

The market demonstrated healthy momentum during 2025 as industrial activity strengthened across construction, transportation, manufacturing, energy, and electronics sectors.

The automotive industry remained one of the largest consumers of non-ferrous metals. Aluminum continued replacing heavier materials in vehicle structures to improve fuel efficiency and extend electric vehicle driving range. Copper demand also increased significantly because electric vehicles require substantially higher quantities of conductive materials than conventional internal combustion engine vehicles.

Construction activities further expanded consumption of aluminum extrusions, copper wiring, zinc coatings, and specialized metal components used in commercial buildings, residential housing, transportation infrastructure, industrial facilities, and public utilities.

Renewable energy projects accelerated demand for copper, aluminum, and nickel across solar photovoltaic installations, wind turbines, battery storage systems, charging infrastructure, and high-voltage transmission networks.

Electronics manufacturing continued generating robust demand for refined copper, tin, aluminum, and specialty alloys utilized in semiconductors, printed circuit boards, consumer electronics, telecommunications equipment, and industrial automation systems.

Growing investments in industrial machinery, robotics, aerospace manufacturing, and advanced manufacturing facilities also contributed to broader market expansion.

2035 Forecast

By 2035, the Non Ferrous Metals Market is expected to reach approximately USD 436.72 billion, reflecting sustained investments in industrial development and global energy transition initiatives.

Electric vehicle adoption is expected to remain one of the strongest long-term demand drivers as automotive manufacturers continue increasing production capacity worldwide.

Large-scale renewable energy deployment will require extensive quantities of conductive and corrosion-resistant metals for power generation, storage, and transmission infrastructure.

Urbanization across emerging economies is anticipated to sustain construction demand for aluminum, copper, and zinc products utilized in residential housing, commercial developments, transportation systems, and utility infrastructure.

Growth in aerospace engineering, defense modernization, semiconductor manufacturing, artificial intelligence infrastructure, and advanced industrial automation will create additional opportunities for high-purity and specialty non-ferrous metals.

Circular economy initiatives are also expected to expand secondary metal production as recycling technologies improve recovery rates while reducing dependence on newly mined resources.

Future Outlook

The long-term outlook for the Non Ferrous Metals Market remains highly favorable because these materials are fundamental to virtually every strategic growth sector shaping the global economy.

Rapid electrification, digital transformation, industrial automation, renewable energy expansion, and sustainable infrastructure development will continue increasing consumption across aluminum, copper, nickel, zinc, tin, and other specialty metals.

Manufacturers and mining companies are expected to prioritize resource efficiency, supply chain resilience, digital operations, and environmentally responsible production to address evolving customer expectations and regulatory requirements.

Increasing collaboration between mining companies, metal processors, technology providers, and downstream manufacturers will further strengthen industry innovation and improve long-term competitiveness.

Technology & Innovation

Technological advancement is transforming every stage of the non-ferrous metals value chain, from exploration and mining to refining, recycling, and downstream manufacturing.

Artificial intelligence, machine learning, and advanced geological modeling improve mineral exploration accuracy while reducing exploration costs.

Autonomous mining equipment enhances productivity, operational safety, and equipment utilization.

Digital twin technologies optimize plant operations by enabling predictive maintenance, process optimization, and energy management.

Hydrometallurgical extraction methods improve recovery efficiency while lowering environmental impacts compared with conventional processing techniques.

Advanced recycling technologies are significantly increasing recovery rates for aluminum, copper, nickel, and specialty alloys, supporting circular economy objectives and reducing carbon emissions.

Research into next-generation alloy development continues producing lighter, stronger, and more corrosion-resistant materials suitable for aerospace, electric mobility, renewable energy, and high-performance industrial applications.

Growth Opportunities

Electric vehicle manufacturing remains among the most attractive growth opportunities for market participants.

Expansion of renewable energy infrastructure continues increasing demand for conductive metals utilized in wind turbines, photovoltaic systems, battery storage facilities, and modern electrical grids.

Modernization of aging power transmission infrastructure supports long-term demand for aluminum conductors and copper wiring.

Rapid growth of data centers, artificial intelligence infrastructure, semiconductor manufacturing, and telecommunications networks further expands consumption of high-purity non-ferrous metals.

Infrastructure investments across developing economies continue generating opportunities for aluminum profiles, copper products, zinc coatings, and industrial castings used in transportation, housing, utilities, and public infrastructure.

Technological innovation in recycling and low-carbon refining also creates opportunities for producers seeking to improve operational sustainability while reducing production costs.

Competitive Landscape

Competition within the Non Ferrous Metals Market increasingly centers on operational efficiency, sustainability, technological leadership, resource security, and value-added product development.

Leading companies including Alcoa Corporation, Rio Tinto, BHP Group, Glencore, Southern Copper Corporation, and First Quantum Minerals Ltd. continue investing in mining expansion, digital technologies, renewable-powered operations, advanced refining facilities, recycling capabilities, and strategic acquisitions.

Companies are strengthening supply chain resilience through geographic diversification while simultaneously investing in low-emission production technologies that align with evolving environmental regulations.

Research and development efforts increasingly focus on advanced alloy engineering, lightweight materials, specialty metal processing, and environmentally responsible production techniques to meet future industrial requirements.

Recent Industry Developments

Mining companies continue expanding investments in automation and intelligent mining technologies.

Recycling infrastructure is growing rapidly as circular economy initiatives gain momentum.

Renewable-powered smelting facilities are reducing carbon emissions across metal production.

Battery material investments continue strengthening nickel and copper supply chains.

Advanced alloy development supports electric mobility, aerospace, and renewable energy applications.

Digital supply chain platforms improve transparency, efficiency, and operational resilience.

Professional Conclusion

The Non Ferrous Metals Market is positioned for sustained long-term expansion as governments and industries accelerate investments in clean energy, transportation modernization, advanced manufacturing, and digital infrastructure. With the market projected to increase from USD 260.76 billion in 2025 to USD 436.72 billion by 2035, at a CAGR of 5.29%, non-ferrous metals will remain indispensable to global economic development and industrial innovation.

Future industry leadership will depend on sustainable mining practices, advanced recycling technologies, digital transformation, supply chain resilience, and continuous investment in high-performance materials. Organizations capable of combining operational excellence with environmental responsibility and technological innovation will be best positioned to capitalize on the significant opportunities emerging across the global Non Ferrous Metals Market.